With many countries around the world considering the retirement of quarantine policies, there is begged the question of what shall happen to our nation’s economy in the coming months. The years-long, global quarantine is a multifaceted beast—it was and is a war against humanity’s health, wealth, and faith. Many have posited that the quarantines were perhaps instituted to hide the signs of a soon-to-crash economy, and thus the emergence of our people from lockdowns might have an unfortunately destructive side effect. To answer our questions, let us consult the crystal ball that is the research division of the St. Louis Federal Reserve Bank.

The St. Louis Fed regularly publishes monetary data on its website; economists and savvy citizens routinely analyze this data to predict future conditions of the economy. Some of the most important data sets are M1 and its components.

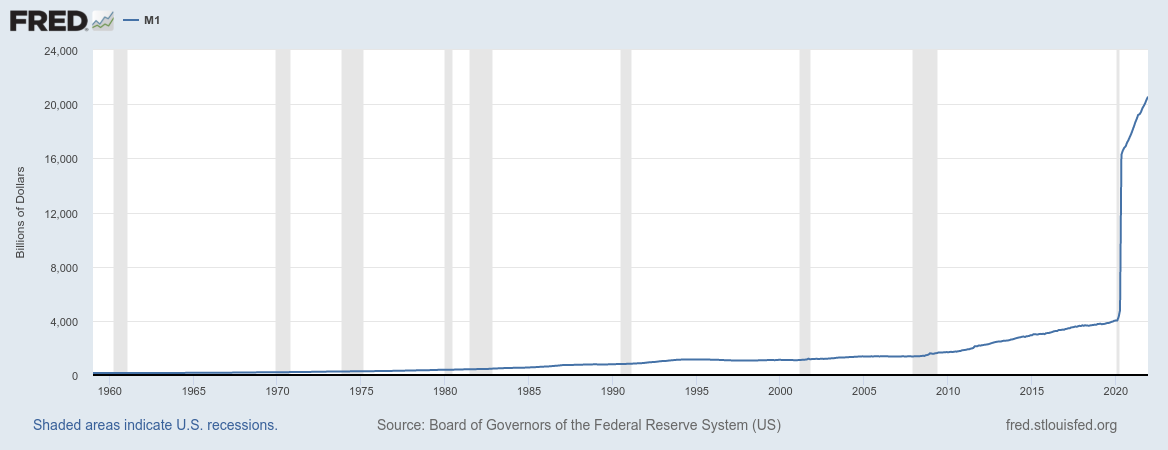

According to the Federal Reserve, M1 Money Stock, or M1, “consists of (1) currency outside the U.S. Treasury, Federal Reserve Banks, and the vaults of depository institutions; (2) demand deposits at commercial banks (excluding those amounts held by depository institutions, the U.S. government, and foreign banks and official institutions) less cash items in the process of collection and Federal Reserve float; and (3) other liquid deposits, consisting of OCDs and savings deposits (including money market deposit accounts).” To generalize, M1 illustrates the amount of dollars that are in circulation.

As one can cursorily gleam from the graph, the amount of USD in circulation has almost quintupled since February of 2021. Where has all this money gone to? Current rates of inflation—as bad as they are—do not reflect what normally occurs when such a voluminous load of currency is printed. Rather than rocketing upwards, inflation just inches along.

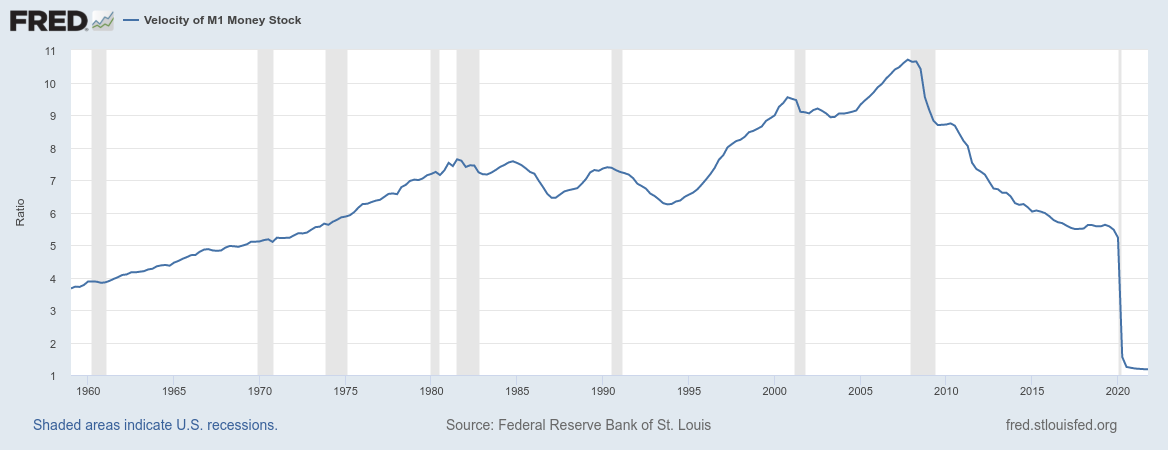

This happens because our nation’s many lockdowns have imbued its citizens with uncertainty of the future; rightly fearing for their safety, many people departed from the rabid spending they enjoyed in years prior. Looking at the graph below, we see that our money velocity (meaning how much of the money in circulation is actually spent) has sharply dropped, and was recently measured as being roughly one third of 1959’s rates during its first quarter. The velocity of money has slowed to a snail’s pace; much of the money that was printed now lies dormant in bank accounts.

Now that some governments are beginning to capitulate on the lockdown question, it is only a matter of time before the propaganda machines follow suit. With specious reluctance, their newsmen will admit that it was a mistake to continue to quarantine for so long. It will be advocated that the citizenry return to a (sub)normal life to allow the economy to recover. Hence, all the money left unspent in Joe American’s savings account will explode outward. The velocity of money will increase; inflation will sharply rise to reflect the trillions of dollars suddenly being introduced into markets. Just like a pyroclastic flow, the ensuing hyperinflation will incinerate everything in its path. Will this cause a social collapse? Only time will tell.

Such hyperinflation might seem impossible if not for the fact that no economic bunglings are new under the sun. Weimar Germany suffered the effects of a similar economic bomb planted by its predecessor state: Imperial Germany fielded quite possibly the strongest army of Europe, and its navy rivaled those of many other powers. The Empire fought WW1 on two fronts in Europe, beat Russia into submission, and almost defeated the rest of the Allies before Woodrow Wilson pulled the U.S. into the war. But these campaigns came at great cost. To accommodate the financial demands of WW1, the Reichsbank abandoned the gold standard and adopted the practice of unchecked Papiermark printing. Like many Americans today, most Germans exhibited fear over the future and were not content to engage in frivolous spending, so the effects of inflation were not easily felt early on. Only after the war—when death was less certain to the public—did “true” inflation begin. Contrary to popular belief, the burden of war reparations was a mere catalyst to Germany’s postwar hyperinflation. The Reichsbank was primarily responsible for destroying the German economy—not the Allied powers. Now, central banking’s same “mistake” is being repeated a century later.

The reader has learned of the queer state of the U.S. economy, what with the country’s banks having printed a seemingly phantom 16 trillion dollars. In parallel, he has learned that the discordant measures of the M1 Money Stock and money velocity must eventually reconcile—which will, of course, have cataclysmic repercussions. Hopefully, his healthy distrust of the internationalists and their banking instruments leaves him questioning the aims of the lockdowns and preparing for the hard times ahead.

Bent, Marty. TFTC, 11 May 2021, https://tftc.io/content/images/2021/05/wheelbarrow-wallet.png. Accessed 14 Feb. 2022.

Federal Reserve Bank of St. Louis. “M1.” Federal Reserve Economic Data, 25 Jan. 2022, https://fred.stlouisfed.org/series/M1SL.

Federal Reserve Bank of St. Louis. “Velocity of M1 Money Stock.” Federal Reserve Economic Data, 27 Jan. 2022, https://fred.stlouisfed.org/series/M1V.